From Barriers to Breakthroughs:

Innovation in Credit Risk Assessment for Immigrants in Canada

While immigrants play a pivotal role in Canada's economic growth and cultural vitality, they face significant barriers in accessing the financial products necessary to build wealth and secure their future.

This report explores the barriers newcomers face in accessing credit, and opportunities for governments, financial institutions, settlement agencies, fintech, investors and funders, and community organizations to better respond to this growing segment of the population.

Newcomer population is growing, with significant economic contributions.

As of 2021, immigrants constitute 23% of Canada's total population, totaling over 8.3 million individuals. (Statistics Canada, 2021)

Projections indicate that immigrants could make up 28.4% of Canada's population by 2031 and 31.8% by 2041. (Government of Canada, 2024)

75% of Canada’s population growth comes from immigration, mostly in the economic category. (Government of Canada, 2022)

There is an opportunity to transform newcomer financial integration in Canada.

54.6% of Canadian-born individuals have mortgages, while only 12.3% of recent immigrants in the same age group have mortgages. 42.9% of Canada-born individuals have vehicle loans, while only 14.5% of recent immigrants in the same age group have vehicle loans. (Statistics Canada, 2023)

Interac survey reveals that 81% of newcomers expressed interest in online courses covering Canadian banking basics. (Interac, 2024)

Immigrants account for 32% of employer business owners, creating vital jobs in various sectors. (Government of Canada, 2024)

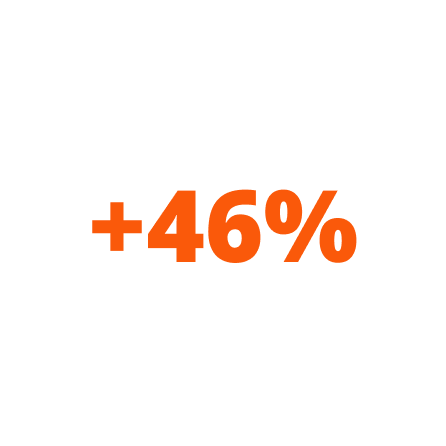

The volume of credit originations by ‘New-to-Canada’ consumers grew 46% YoY from 2022 to 2023. (TransUnion, 2024)

Key insights

Credit access is often framed as a personal responsibility—establishing a score, managing debt, and building a history. However, for many newcomers, the system presents significant obstacles. This section examines what newcomers face. Drawing on data from primary and secondary research, it highlights areas where current systems fall short and identifies opportunities for targeted, practical improvements.

Branch-Level Implementation Gap

Credit approval for newcomers varies by branch location, with higher success rates in newcomer-dense areas.

Informal Networks Play a Double-Edged Role

Community networks provide critical financial guidance, but also perpetuate outdated or incorrect information.

Cultural Financial Behaviours Impact Credit Assessment

Traditional credit scoring models often overlook different cultural financial habits. Newcomers from savings-focused economies may be misclassified as high-risk due to limited credit history, despite strong repayment behaviours.

Persistent Financial Literacy Gaps

Financial literacy gaps affect many newcomers, including those who are highly educated, influencing credit use and debt management.

Settlement vs. Career Focus Mismatch

Financial programs often prioritize career development while overlooking critical early settlement needs, including housing, transportation, and basic living costs.

Marketing to Practice Gap in Credit Offerings for Newcomers

While major banks advertise attractive credit products for newcomers, they often offer lower credit limits and do not disclose the scope of documentation needed for approval.

Digital Access Challenges for Newcomers

Credit card providers' reliance on digital channels, without personalized guidance, creates significant accessibility barriers for newcomers, especially when they are seeking entry-level credit-building tools.

Credit Access Is a Gap in Newcomer Research

Credit access is increasingly recognized as a foundation for successful integration alongside employment, language acquisition, and credential recognition. Yet it remains largely overlooked in settlement research.

Credit barriers are not always visible in aggregate statistics. They show up in everyday decisions, whether to rent or buy, take a job across town without a car, or open a business without a loan. For newcomers, these financial choices shape the trajectory of integration. However, the system may not fully reflect the complexity of their starting points and lived experiences.

In the following section, we follow the journeys of three newcomers: Paula, a permanent resident; Oumarou, a temporary worker; and Muchen, an international student. Their experiences highlight how Canada’s credit system interacts with different newcomer pathways, illustrating where the system supports and where barriers persist.

Credit Access Journey of Three Newcomers

Credit Products For Newcomers To Canada

Did you recently move to Canada? Discover credit products to help you build and enhance your credit profile. From daily expenses to buying a home, these credit products from Canadian banks and community programs will help you get there.

Acknowledgements

This project was made possible through the generous support of the World Education Services (WES) Mariam Assefa Fund (MAF), which is committed to supporting newcomers and helping them integrate into Canadian society. We extend our gratitude to the community organizations, financial institutions, and scholars who participated in stakeholder engagement interviews, sharing their time, expertise, and insights. We also thank the individuals and organizations who provided critical feedback, guidance, and encouragement throughout this process.

Our work takes place on the traditional territory of the Mississaugas of the Credit, the Anishinaabe, the Chippewa, the Haudenosaunee, and the Wendat peoples, in the area known as Tkaronto, now called Toronto. This land, covered by Treaty #13 and the Williams Treaties, has long been a gathering place for many First Peoples and remains home to diverse First Nations, Inuit, and Métis communities. As an organization dedicated to shifting capital flows toward underfunded communities, New Power Labs is grateful to work alongside Indigenous communities in our research, practices, and partnerships.